by Dominique Lapointe

Following last Friday’s release of Statistics Canada’s September 2017 Labour Force Survey (LFS), the Institute of Fiscal Studies and Democracy (IFSD) has updated its Canada JØLTS analysis for August 2017.

Economic and Monetary Implications

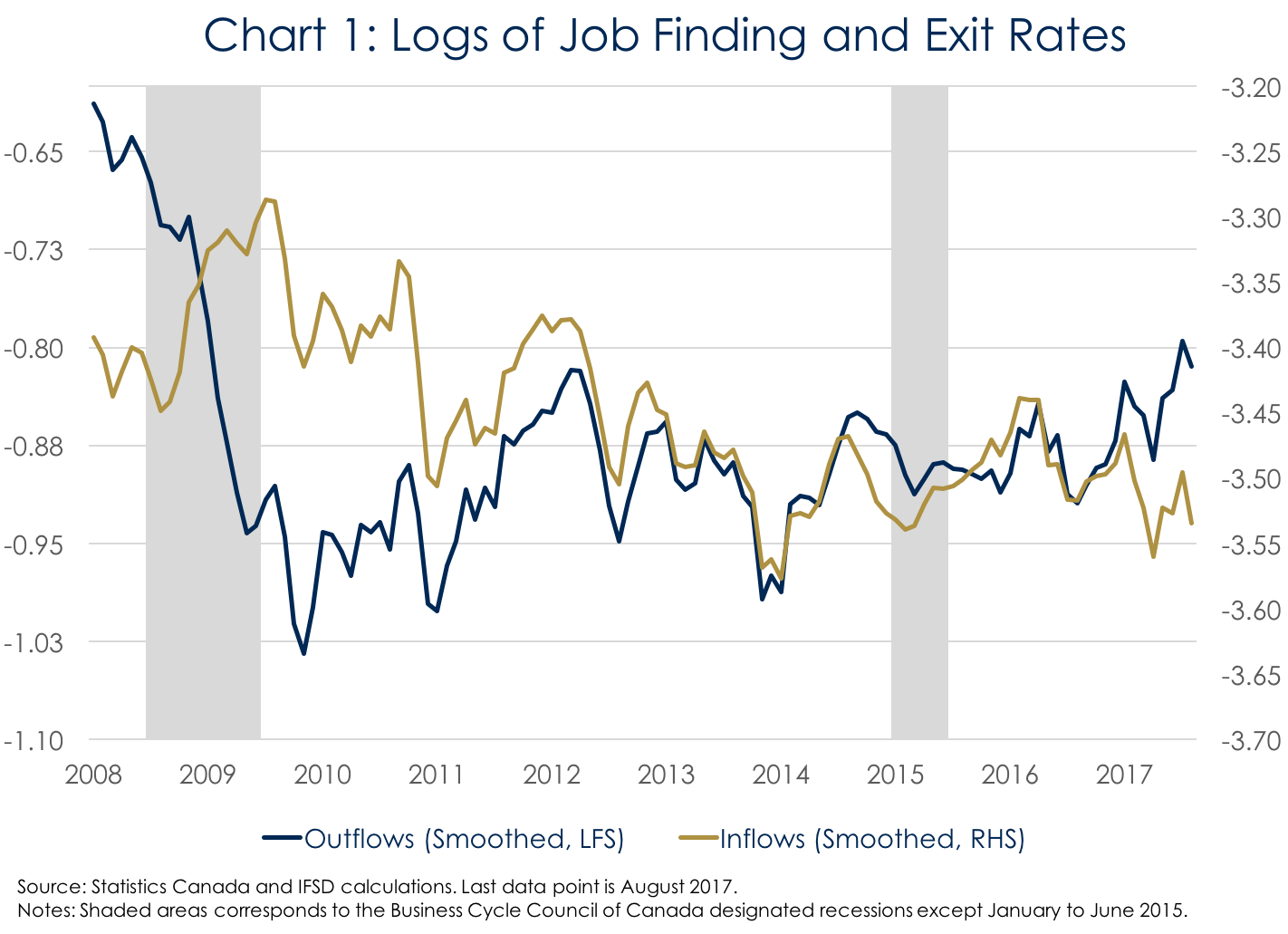

In August 2017, the unemployment outflow rate decreased by 14% and the inflow rate decreased by 17% (Chart 1).[1] These latest unemployment inflows and outflows support the view that the acceleration in economic growth in Canada has likely peaked, although is remains solid.[2] The movement in the inflow rate observed in the last couple of months is partly explained by a slight uptick in the short-term layoff rate, albeit from an all-time low earlier this year (see Chart 2 and section below). More importantly, the outflow rate ticked down in August, but is still hovering around post 2008-09 recession-highs. This suggests very strong demand for qualified workers e.g. a tighter labor market. In fact, the national unemployment rate is at its lowest level in nearly a decade (6.2% in September). As a consequence, it is no surprise to observe a recovery in wages across the country. The average hourly wage is up by 2.2% year-over-year in September, the highest pace since April 2016. Consistent with the IFSD’s latest economic and fiscal forecast, stronger wages should fuel a pickup in core and total inflation going into the next year. This is corollary to the view that the output gap in Canada is basically closed. Nonetheless, the Bank of Canada (BoC) is likely to assess the economic impact of its recent interest rate hikes before deciding to tighten monetary policy again. Recent speeches have also suggested that the BoC may revise its estimate of potential GDP upward in its October 2017 Monetary Policy Report, thereby lowering the Bank of Canada’s estimate of the output gap – an important indicator of impending inflationary pressure. Therefore, the IFSD has the view that the next interest rate hike is not coming before January 2018.

Focus on Quits and Layoffs

As mentioned in Section II of the first Canada JØLTS report, people flowing into unemployment (the inflow rate) are restricted to respondents who either lose their job or quit their job. Using the LFS microdata file, quits and layoffs ratios, defined as newly unemployed who either quit or lost their job as a share of total employment, are calculated.[3]

National Perspective

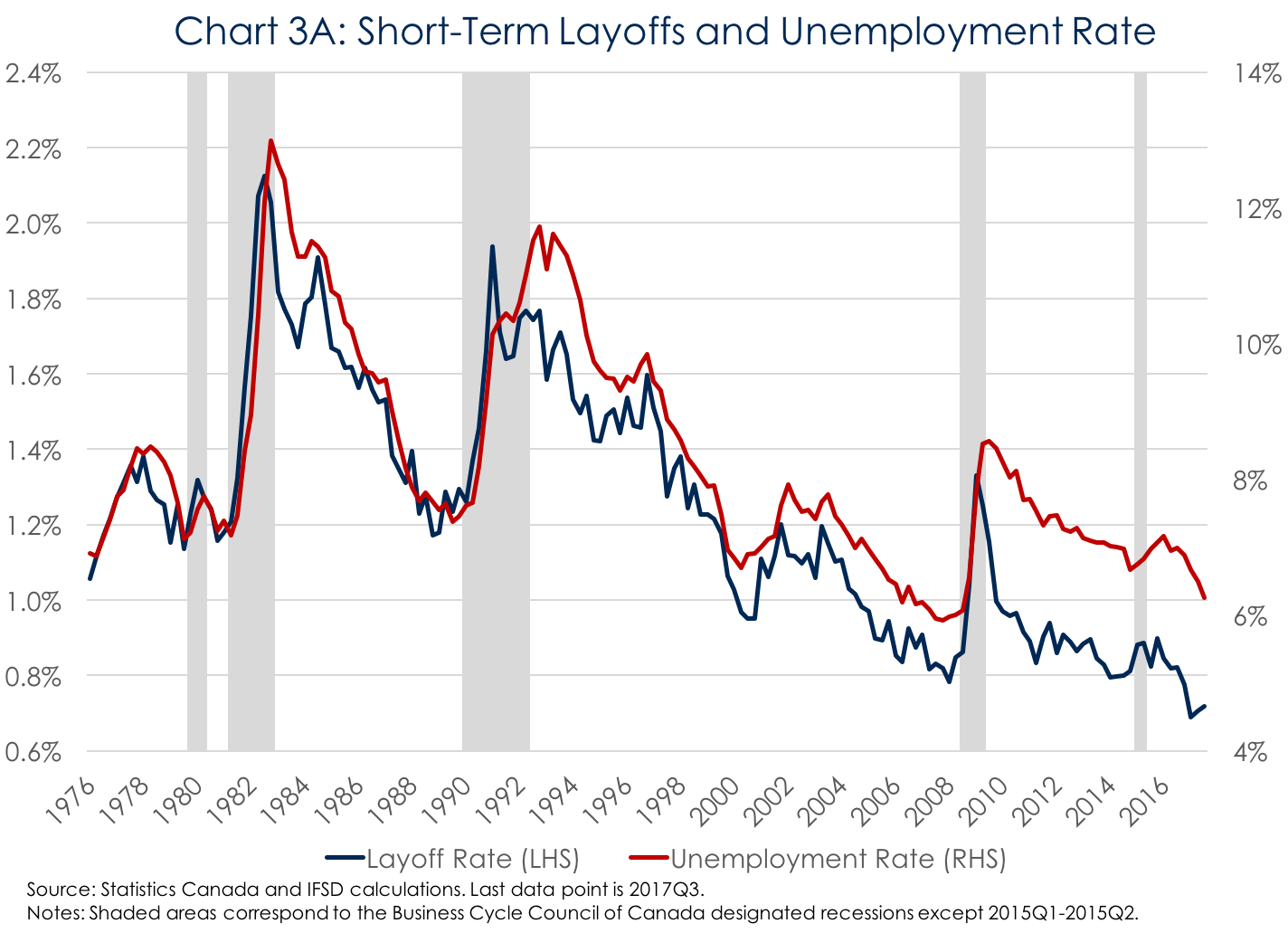

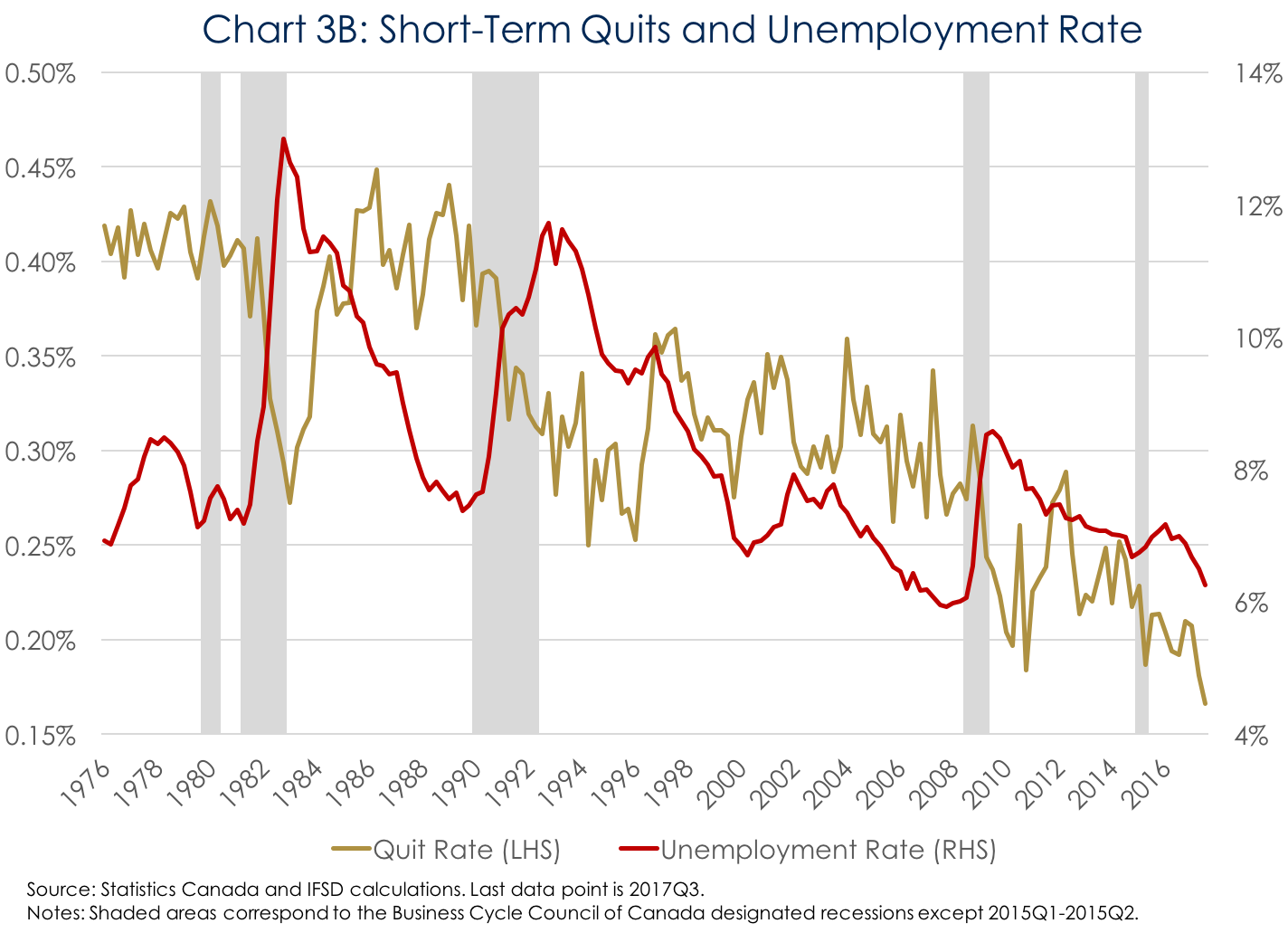

Chart 2 shows the short-term quits and layoff rate (as a share of employment) in Canada since 1976, which can be used as a proxy to explain movements into the unemployment pool.[4] A few interesting observations can be gleaned from the above:

- The short-term layoff rate (left side of the chart) is consistently lower than the short-term quit rate (right side of the chart), suggesting that, in general, layoffs explain more of the inflows into unemployment than do quits. However, it is important to keep in mind that both the unemployment flows and the quits and layoffs rate do not take into account people flowing in and out of the labour force.[5] In every month, for various reasons including retirement, school, or travel, workers quit their job and go out of the labour force. Those women and men are not included in the IFSD’s unemployment inflows.

- The short-term layoff rate rises rather dramatically during recessions. Indeed, in the 1981-82, 1990-92, and 2008-09 recessions, the short-term layoff rate rose by 0.7 percentage points of total employment on average. On the contrary and as expected, the short-term quit rate falls significantly during a recession as employees observing current economic conditions as well as greater slack in the labour market decide that quitting their jobs to look for other employment opportunities might not be ideal at that moment.

- Another pattern worth mentioning is the timing of the inflows’ movement during a recession.[6] The sharp rise in the short-term layoff rate during a recession happens coincidently with the beginning of the recession. In fact, the rise in the layoff rate even precedes the rise of the total unemployment rate when a recession begins (Chart 3A). Moreover, the former falls quicker than the latter after peak unemployment has been reached.

- Conversely, the short-term quit rate reacts with more delay to the recession, falling drastically only after a few quarters, on average (Chart 2). Consistently, the short-term quit rate follows more closely the peaks and troughs of the unemployment rate (Chart 3B).

Examining history, the short-term quit rate now stands at 0.20% in September 2017, lower than its post-recession average (Chart 2). The short-term layoff rate is 0.7%, also lower than its post-recession average. That pattern is also consistent with a relatively low rate of inflows, as seen in Section II of the IFSD’s first Canada JØLTS report. As such, the recent movement in the unemployment rate continues to be driven mostly by a stronger outflow rate, or the relative speed at which unemployed people find jobs. This points to strong demand on the part of employers, suggesting that the Canadian economy may be coming up against capacity constraints – a views supported by the most recent output gap estimates from the IFSD and BoC.

Provincial View

Provincially, the short-term layoff rate in Ontario has been continuously trending towards historical lows since early 2014, consistent with the pick-up in economic activity in the province around that time (Chart 4A). At 0.6% in the third quarter of 2017, it now sits below the national average (0.7%). The story is similar in Quebec. However, the drop in the short-term layoff rate happened more recently, around the beginning of 2016, and is now in line with the national average (Chart 4B). Finally, the short-term quit rate in Quebec has recovered from an all-time low of 0.10% in the second quarter of 2017 to 0.16% in the third quarter, also in line with the national average.

Conclusion

In summary, the short-term quit and layoff rates are useful complements to the unemployment inflows since they provide insights on what is driving workers’ movement from employment into unemployment. Moreover, it seems that during economic downturns, the short-term layoff rate will adjust more quickly than the quit rate and the overall unemployment rate. As such, the IFSD will continue to monitor and update monthly those complement indicators to the labour force survey’s headline unemployment rate and employment level.

[1] To see through the volatility, Chart 1 is presented as a 3-month moving average.

[2]The inflow rate represents the “speed” at which people enter the unemployment pool while the outflow rate represents the “speed” at which unemployed people find a position. See Section II of the report for a complete definition of the inflow and outflow rate.

[3] The labour market model used to estimate the inflow rate does not allow for the separate identification of a layoff rate and a quit rate. They need to be identified separately. Because of that, the interpretation differs: the inflow rate represents the “speed” at which people enter the unemployment pool while the quit and layoff rate are the incidence of workers who either lost or quit their job to become unemployed, relative to all workers (employed people). That methodology is akin to the one used to determine U.S. JOLTS quits and layoffs/discharges rate. Please see: https://www.bls.gov/news.release/jolts.tn.htm for more details.

[4] LFS respondents who declared to have been without a job and actively looking for one for the last four weeks or less.

[5] See section II of the report for more details about the assumption related to the flows in and out of the labour force.

[6] The beginning and end dates of the recession periods are determined by C.D. Howe Institute’s Business Cycle Council, with the exception of the economic slowdown of 2015.